Farmland biodiversity – where next for market-based mechanisms?

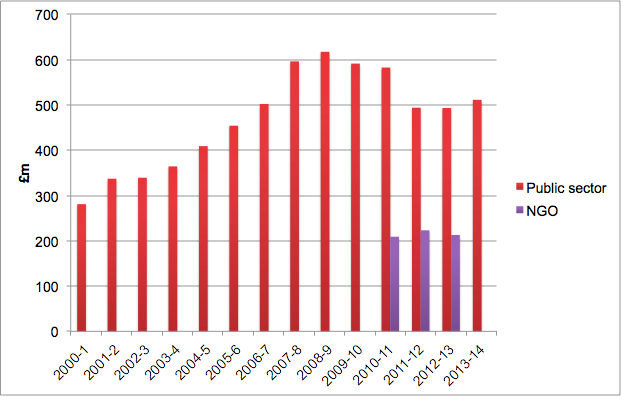

Exactly a decade ago I got my first job in the agri-food sector as a farm conservation advisor. A typical day saw me surveying farm habitats and helping land managers integrate biodiversity into their day-to-day business practices – nearly always financed by EU agri-environment schemes (AESs) or charitable trusts. Public sector and NGO expenditure on UK biodiversity peaked in 2008-9 and now stands at approximately £750 million per year (see Figure 1 below).

Figure 1: Investment in biodiversity in the UK by public sector and NGOs(1)

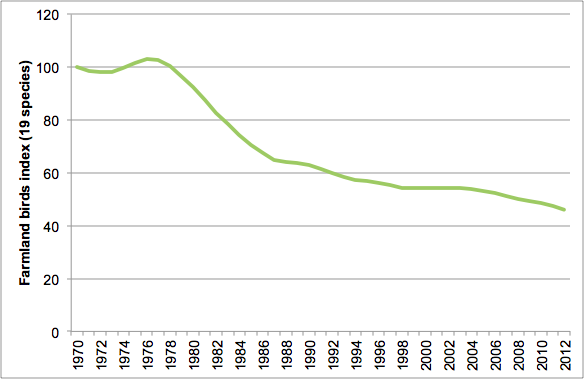

Given the prevailing national and international political climate, it’s unlikely that public funding of UK biodiversity will reach those levels again any time soon, however the core challenges remain. Despite billions of pounds of public investment in a set of very complex policy tools, the declines in many UK biodiversity indicators have not been halted, let alone reversed (see Figure 2 below).

Figure 2: Farmland birds index

Conservation researchers have been trying to establish if AESs are working as intended. Unfortunately the evidence so far has been mixed and inconclusive.

The rise of ‘market-based mechanisms’

Alongside the recent decline in public funding, corporate interest in biodiversity has steadily increased – driven by a growing understanding that business is ultimately dependent on a suite of related ecosystem services (e.g. pollination), as well as a desire to protect corporate reputations from being associated to habitat destruction. To help incentivise the protection and restoration of biodiversity, different market-based mechanisms have been designed and implemented. The majority have focused on creating new markets or transactions by which land managers can get economic benefit from changing practices, such as:

-

Tradeable permits e.g. ‘offsetting’ biodiversity losses caused by construction projects

-

Product certification e.g. LEAF Marque, Conservation Grade

-

Other Payments for Ecosystem Services (PES) e.g. nitrogen trading in Poole harbour

Unfortunately there is no reliable data on the scale of private sector investment in UK biodiversity via these and other mechanisms (including self-financed work by farmers, food supply chain producer groups, etc.). And while it is probably on the increase, we estimate that investment is an order of magnitude lower than current expenditure by the public sector and NGOs(2). It would also be fair to say that none of the approaches above have proved themselves so far. This could be down to the relative immaturity of the tools – and there is undoubtedly room for improvement – we think particularly through more entrepreneurial PES schemes (such as those being piloted by 3Keel and the Woodland Trust near Bolton).

Given this context and experiences to date we think it’s a good time to stand back and have a cold hard view at how the private sector – or market mechanisms – can most effectively incentivise the desired biodiversity and ecosystem service outcomes.

Biodiversity management in the UK – a landscape of competing incentives

The complexity of existing farmer incentives and the landscape-scale of ecosystem service processes has major implications for the effectiveness of different market mechanisms. A glimpse into some of these implications can be seen in a peer reviewed analysis of public and private sector conservation schemes in the UK. The research found that, while there was greater habitat diversity on farms with private sector certification compared to publicly-funded ‘entry level’ agri environment schemes, it was difficult to say whether this was down to the adoption of the private sector standard or the farm’s participation in ‘higher level’ agri environment schemes. My instinct is that the amount of monitoring and evaluation needed to make confident statements about the relative contribution of multiple private, public and third sector incentives will be uneconomic and a potentially a worrying distraction. Put another way, it has been possible to compete and compare on the basis of activity (e.g. areas of field margins created) but I suggest impractical/impossible to do so on biodiversity outcomes (i.e. improvements in farmland bird numbers in a particular landscape or region). As stakeholders increasingly expect the impact of sustainability initiatives to be judged on outcomes this aspect of biodiversity will become ever more obvious. Competing on farm-level conservation actions will be less and less credible.

On a more practical note, if the private sector’s strategy is to set more standards that require similar or competing conservation management measures to those being incentivised by billions of pounds of NGO and public funding, this instinctively doesn’t feel like a route to delivering a step-change in biodiversity improvements. What will the marginal impact of these additional incentives be?

Harnessing market-related incentives

Given the above challenges we need to explore novel market-based mechanisms for incentivising improvements in biodiversity – and sustainable natural resource management more broadly. 3Keel is exploring what this means in practical terms, however I believe that new mechanisms will have the following core characteristics. They will:

-

Operate at landscape or regional scales. Because biodiversity and natural processes span large geographical ranges, researchers and policymakers are increasingly calling for action at ‘landscape’ or regional scales. This scale also aligns with other, more local, governance structures and enables the identification of key actions and decision-makers (supply chains are quite intangible concepts). While plenty of landscape projects have been funded in the UK, the mechanisms for getting meaningful engagement by large businesses are still in their infancy. Having said that, the private sector is making noises about intervening at these scales (such as Unilever’s recent pledge to source from regions which meet deforestation standards)

-

Focus on conservation outcomes and encourage bottom-up solutions. The complexity and variability of the challenges, I believe, requires that local stakeholders are best placed to identify who needs to act and what needs to be done. Land managers should be freed from prescriptive management requirements and instead judged on regional environmental outcomes. To achieve this funding needs to be invested in monitoring environmental indicators using emerging low cost monitoring techniques and strategies (e.g. use of remote sensing, Internet of Things, crowd sourcing, Big Data, etc.). These more flexible approaches need to be combined with standards and certification that cover the critical areas of business performance e.g. food safety, labour standards, basic pollution control measures, etc.

-

Identify and communicate hidden economic and social risks. While the importance of ecosystem services is understood by researchers, policymakers and enlightened businesses, the short/medium term implications of unsustainable resource management are not being communicated in a way that really speaks to investors, asset owners, customers, etc. The effectiveness and impact of the ‘business case’ for action needs to be further strengthened. For example, financial institutions such as the Bank of England, are increasingly interested in the disclosure of environmental risks. This ties into the growing ‘transparency’ agenda and interest from investors, customers and users of the multiple goods and services that flow from natural resources.

Overall, it’s time for some smarter, simpler thinking to get the land use outcomes that society wants and needs. Complex interventions in complex systems can be costly and deliver unintended outcomes.

To find out more about 3Keel’s innovation work on this topic please contact 3Keel Partner Richard Sheane.

1 JNCC data http://jncc.defra.gov.uk/page-4251. No data on NGO investment prior to 2010-11

2 I estimate it is probably of the order of £50m per annum. Based on a comparison of the area of farmland being managed for biodiversity under ‘voluntary’ measures compared to that under agri-environment schemes

![]()

The complexity of existing farmer incentives and the landscape-scale of ecosystem service processes has major implications for the effectiveness of different market mechanisms.